Showing posts with label european union. Show all posts

Showing posts with label european union. Show all posts

18 February 2017

15 February 2017

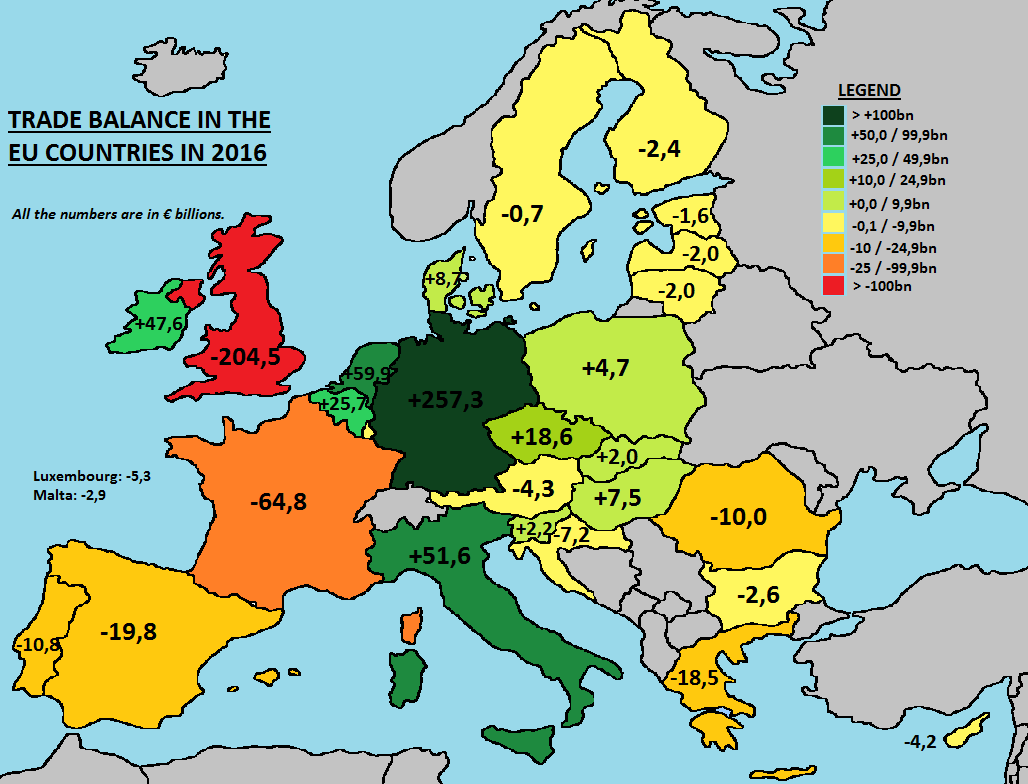

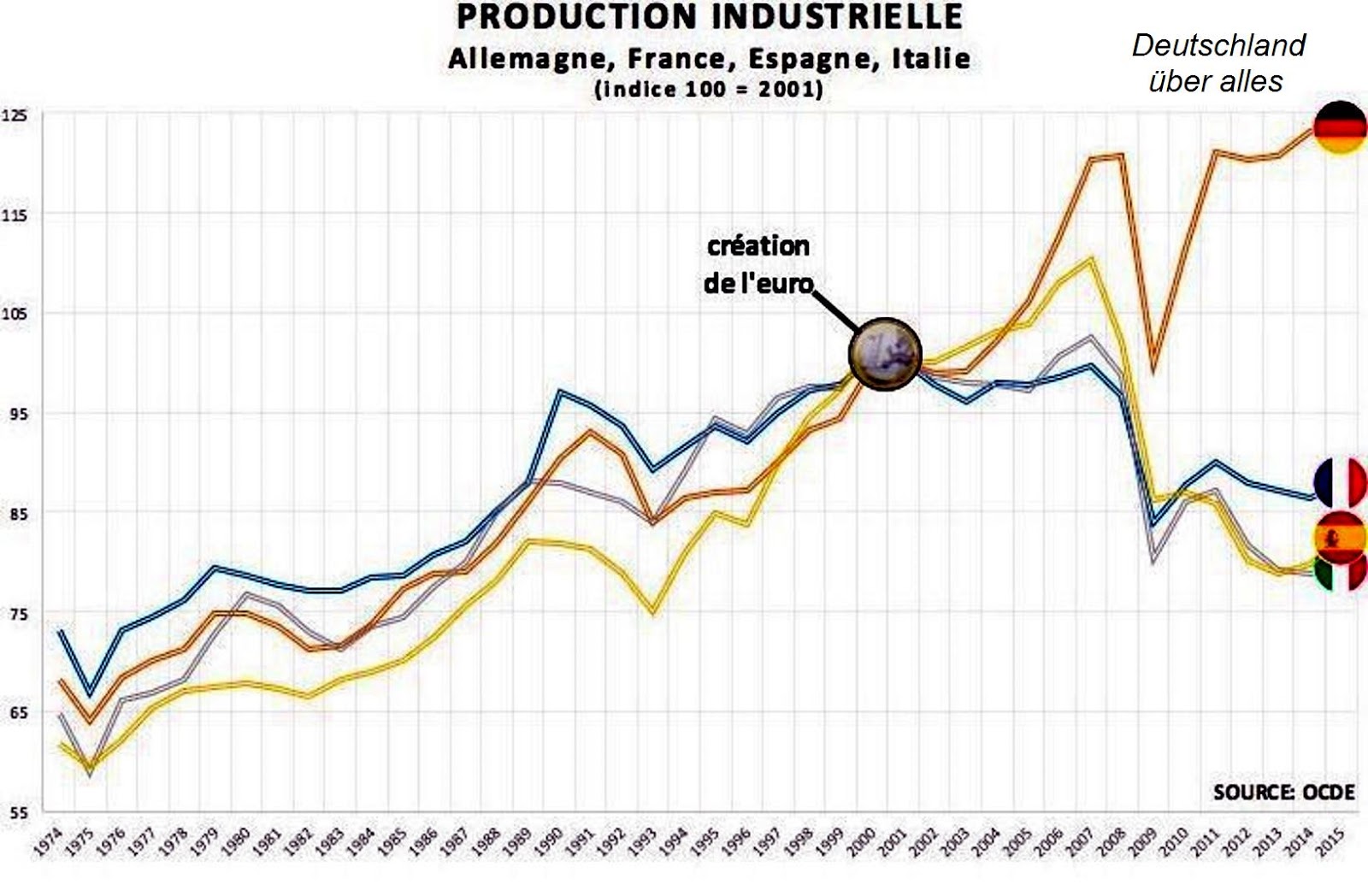

The Failure of the European Monetary Union In One Graph

This is why a wave of populism is sweeping the EU bureaucrats aside.

A similar wave of populism is underway in the US.

The reasons for it are obvious: the abuse of the law and of power in the service of a 'fortunate' few in a self-selected class of meritsocrats and their anointed.

As the pigs proclaimed in Animal Farm, 'all animals are equal, but some are more equal than others.'

The credibility trap prevents the establishment and their enablers from discussing the core issues, and often even acknowledging that there is any problem.

Today's Yellen testimony and questioning before Congress was a nice example.

The Congress critters are craven except in a spirited defense of their own big money backers and sinecures, the general public and middle class be damned.

01 February 2015

France Prepared To Support Greece in Debt Negotiations

Support, whatever that means.

The negotiations and discussion surrounding the Greek debt issue are not straightforward nor transparent.

People will tend to project their own opinions on to this since it is rather complicated, especially for those not familiar with international politics.

There are a number of issues involved, and a number of players, some with their own interests and agendas that intersect enough with this to bring them into the discussions.

And like most political situations of complexity the ultimate resolution will likely involve some compromise. So those who prefer to enhance their reputation by second guessing will almost certainly have some opportunity to say 'I told you so.' Like so many stock forecasters, they write their hits in marble, and their misses in sand.

There are a number of issues involved, and a number of players, some with their own interests and agendas that intersect enough with this to bring them into the discussions.

And like most political situations of complexity the ultimate resolution will likely involve some compromise. So those who prefer to enhance their reputation by second guessing will almost certainly have some opportunity to say 'I told you so.' Like so many stock forecasters, they write their hits in marble, and their misses in sand.

In addition, I cannot stress enough that relying on only one category of mainstream media sources on this entire topic can be highly misleading.

The amount of spin and perception management being generated even by 'name' media sources these days is pronounced. Remember the stories being put out earlier this month that Russia was on the ropes, and was selling its gold to meet its reserve obligations?

And there are global macro and political issues enough so that the neo-liberal establishment will be keenly interested in becoming involved in this, fear contagion and the 'domino effect' not only in Europe, but in their own countries.

And quietly, almost unnoticed, China and Russia keep accumulating gold bullion.

Such are the times of currency wars. And I think we might know to whom most of the Western commercial press owes their allegiance. And they are not the only ones.

But they are unusually shameless considering the image that their PR has created. I have not seen this much blatant propaganda in the major news in a very long time, probably not since the early part of the Vietnam war.

France ‘prepared to support Greece’ in debt renegotiations01/02/2015France’s Socialist government offered support Sunday for Greece’s efforts to renegotiate debt for its huge bailout plan, amid renewed fears about Europe’s economic stability.The backing was a victory for Greek Finance Minister Yanis Varoufakis, holding talks with European officials to push for new conditions on debt from creditors who rescued Greece’s economy to save the shared euro currency. Worries have mounted that Greece’s new far left government might not pay back its debts.Varoufakis is also visiting London and Rome – and said Sunday that he would visit Berlin. The German government has been particularly angry at the new Greek government’s position and bluntly rejected suggestions that Greece should be forgiven part of its rescue loans.Varoufakis insisted that Greece wants to pay the money back, but said he wants new terms and new negotiating partners, arguing that “it’s not worth” discussing with the so-called “troika” of creditors who set the strict terms for Greece’s rescue.France’s Socialist leadership, whose president has campaigned against austerity, presented itself Sunday as a possible mediator between Greece and creditors.French Finance Minister Michel Sapin insisted his country wouldn’t support canceling the debt, but offered support for a new timeframe or terms.“France is more than prepared to support Greece,” Sapin said after meeting Varoufakis, saying Greece’s efforts to renegotiate were “legitimate.” Sapin urged a “new contract between Greece and its partners.”Greek Prime Minister Alexis Tsipras and his new government have worried financial markets and German and other European officials by pushing to scrap painful budget cuts and rethinking the debt. Tsipras sought to calm worries over the weekend after days of increasingly heated discussions.Varoufakis announced that he has retained financial consultants Lazard as advisers to the Finance Ministry on issues of public debt and fiscal management. The socialist PASOK party, which ran Greece during part of its debt crisis, praised the decision, noting that then-Finance Minister Evangelos Venizelos also hired Lazard advisers when he negotiated with private bondholders in 2011-2012.

26 September 2013

The Financial States of America and Why the European Union Is Inherently Unstable

I am including this because it shows the economic diversity in growth and wealth amongst the States.

And they all function under a common currency. Why does this work whereas the Eurozone is having such problems?

That is because with a common currency union, a political and fiscal union are required as well. This is a hard lesson from monetary theory and history.

When you have a fiat system with a central authority setting policy according to economic conditions over a geographic area in which there is diversity, there must be fiscal policy and transfer payments to 'even out' the effects of that monetary policy.

That is why the European Union is inherently unsustainable, because it is a monetary union without a public policy and fiscal union.

The EU cannot possibly create the appropriate single government, without undue hardship. So they must consider allowing the individual countries or regions to conduct their own monetary policy and have their own currency and exchange rates.

Source: Financial States of America

This chart is from Moneychoice.org. They are responsible for the data and the figures.

18 March 2013

Cyprus Update - The Calm Before the Storm - One Europe?

I am sure you are aware of the events unfolding in Cyprus, at least if you follow the financial news and the internet.

The vote in the Cyprus Parliament has been postponed until Tuesday, most likely because the votes were not there to pass a resolution that was acceptable to the EU.

The bank holiday has been extended to Thursday, and it is doubtful they will reopen until the Parliament has sorted out a plan of action. The shutting of the banks while the politicians wrangle over the details of the confiscation is not designed to heighten confidence.

As you may recall, the President of Cyprus, Nicos Anastasiades, a member of the conservative Democratic Rally (DISY) party, was elected in February of this year with about 58% of the vote. He is known as a blunt, chain-smoking 'strong man' with strong ties to the right wing politicians of Europe. Indeed, these connections and his promise of a solution favorable to Cyprus were strong factors in his recent electoral victory.

The extenuanting factors here are that Cyprus is viewed as a bellwether for Italy and Spain. There are many who would dispute this, and point to the particularities of the size and structure of the Cyprus banking sector. But there is a widespread perception that the heavy hand of Germany is running the EU these days, and prior pledges and principles cannot be trusted if the central rulers of the EU are willing to confiscate the insured deposits of private citizens, no matter how they try to rationalize it.

I tend to view this as the overall progress in the foregone drama of an inherently unstable European Union that has fallen into a financial plutocracy. Any actions they take now are merely delaying the inevitable. And the consequences for the global financial sector are profound.

The EU and the Fed may be able to paper over the problems and achieve an uneasy stability that could last a year or two, but without profound changes to the European financial arrangements that include transfer payments, a single currency spanning such diverse national economies is inherently unstable. It is the child of the overreach of bureaucratic arrogance and economic fairy tales.

This *could* be a rather clever move to force at least a portion of Europe into a single political government of twelve or fifteen members, but I hate to give the plutocrats that much credit for planning.

I know there is and has been talk for quite some time of dividing the world into five or six major spheres of political influence, including North America and a few South American client states, Europe, Russia, China, and Japan. The particularities of southeast Asia and the Pacific are very much in play, along with the status of various economic colonies in the Third World including Africa. India and Australia are major outliers. The UK has been particularly troubled by its relatively minor role, and aspires to be the financial center and interface to the world for the rest of Europe.

Whether any of this happens or not is very much open to question. But the establishment of a 'new order' in the world has quite a few globally powerful adherents who are willing to work for this in the long term. It should be remembered that the fashions of 'centralization and decentralization' of power have their swings, seemingly like a natural ebb and flow over time, quite similar to what we often see in the corporate world.

09 May 2012

The Question Is 'How Best To Default' and Not 'How Best to Maintain the Unsustainable'

"The issue which has swept down the centuries and which will have to be fought sooner or later is the people versus the banks."

John Dalberg Lord Acton

Greece is the most awkward of the EU countries by far in terms of economic fit.

There is no conceivable way that Greece can remain in a single currency union without regular transfer payments from the rest of the EU to compensate them for holding a highly overvalued currency relative to their own economy, geared more to the Germans and the French.

The problem is that the political structure of the EU does not accommodate this sort of adjustment, and within the current political character of the EU the notion of such payments is abhorrent. The Germans, for example, have never thought of themselves as 'fellow Europeans' with a country such as Greece, and the economic structure of Europe does not easily lend itself to de facto payments.

Compare this to the US, with Greece as one of the poorer states, which receives much more in tax receipts and federal projects than the tax revenue that they send in.

It 'works' in the US because it is one nation by structure and by character. Despite their regional differences, most Americans can comfortably think of themselves as 'Americans' first wherever they might live. Unless they are urban cowboys from Texas perhaps (lol).

Every time I look at the structure of the EU politically and economically with the one currency I ask myself, "What were they thinking?" There is no way to go by halves with a single currency and no accompanying political union.

But this is the sort of building by half measures to which Europe has often been susceptible. Bureaucrats love compromise, often blinded to how weak and unsustainable that compromise might be. Any deal is not always better than 'no deal,' except to the dealmakers.

So either the EU will change politically, which is highly unlikely, or Greece will leave the EU and once again obtain its own currency.

I think that outcome is almost predetermined. Now it is only a question of 'how' and mostly with regard to the possibilities of cross-contamination in the financial realm.

The best solution is for Greece to simply leave the EU, default on its debts, nationalize its banks, and restore the drachma at some highly devalued level. I think Iceland shows the way in this. This will greatly disappoint the private financiers who are licking their lips at the prospect of buying real national assets on the cheap with overvalued paper.

The worst problems will be for the European banks who hold Greek debt.

I would consider seriously an action that allows the banks to simply write off the Greek debt, and declare all CDS on Greek sovereigns null and void except for those who actually hold Greek bonds, to the extent of fifty percent of their nominal value.

If this is not workable, I would suggest that Europe also should nationalize and restructure their banks. This is what ought to have been done in 2008, and much of what has been done since then is waste. The greatest resistance to this will come from the one-worlders and their friends in the Anglo-American financial cartel. They would also like a single world currency, which is unworkable without government by a 'new world order.'

The absolute worst model is the American way, in which the banks are given the keys to the Treasury, the markets, and the political process, and allowed to do as they please, while maintaining a thin facade of legitimate government by the people.

They may as well get this done, and stop the charade. And then the rest of the world can begin thinking of how they might reform international trade, replace the existing reserve currency system, and bring the Anglo-American privateers back under control once again.

21 July 2010

Fiscal Union Is Implied if Not Required by a Monetary Union

In 1991 during a visit to Brussels for a discussion of the EU '92 event with some of the bureaucrats engaged in planning there, my old economics professor predicted that no matter what they said, a monetary union implies a fiscal union, greater than the targets and harmonisation which they would admit, men being the creatures that they are.

It makes sense when one understands monetary policy and its theory, and the implications it has in restricting the freedom to save or spend as one may wish to pursue as a fact of fiscal policy.

Here is a story below in which France and Germany discuss their moves to bring more uniformity to their fiscal policies. Quite frankly I am surprised that it has taken this long for it to happen. With the financial crisis tearing down the facades, the extend and pretend policies of the EU have collapsed, and the cheating behind their targets have been exposed for the farce that they are.

And by extension, if one's monetary and fiscal policies are no longer their own, but shared with another and intimately bound by a common currency, then a greater political union and independent governance is a moot point.

This is what my old professor predicted in 1991. And on the train ride back to Paris he said, "Watch what happens if there is a move to establish a single world currency that is a sovereign instrument, and not merely a reference to a basket of currencies and commodities. And then he quoted the famous observation from Mayer Rothschild: "Give me control of a nation's money and I care not who makes the laws."

It has been many years since we have spoken. He was tottering towards his retirement then, and I suspect that he is smiling at all these developments from some better and kinder vantage now, as I know he would be even if it was a profane preference. It was always his first joy to probe the subtle mysteries of money, and how they related to the political follies of men. It was he who first infused me with an interest in the study of money, an aspect of macroeconomics which bordered on his obsession. And it opened a new world to me, and an endless fascination with what is difficult, but so wonderfully, and often subtlety vast.

"Much have I travell’d in the realms of gold,

And many goodly states and kingdoms seen;

Round many western islands have I been

Which bards in fealty to Apollo hold.

Oft of one wide expanse had I been told

That deep-brow’d Homer ruled as his demesne;

Yet did I never breathe its pure serene

Till I heard Chapman speak out loud and bold:

Then felt I like some watcher of the skies

When a new planet swims into his ken;

Or like stout Cortez when with eagle eyes

He star'd at the Pacific--and all his men

Look'd at each other with a wild surmise--

Silent, upon a peak in Darien."

John Keats, On First Looking Into Chapman's Homer

LesEchos.fr

France

et Allemagne s'attaquent à l'harmonisation de leur fiscalité

La bonne gouvernance européenne implique, notamment, l'harmonisation des politiques fiscales. Paris et Berlin en font leur credo, qui ont fait un pas ce mercredi vers une convergence de leurs systèmes fiscaux, à l'occasion de l'invitation au Conseil des ministres français du ministre allemand de l'Economie et des Finances Wolfgang Schäuble.

L'objectif est que « nos deux gouvernements soient ensemble en mesure de prendre des décisions pour aller vers la nécessaire convergence fiscale, tant dans le domaine de la fiscalité des entreprises que dans celui de la fiscalité des particuliers », a annoncé l'Elysée dans un communiqué. « La convergence entre nos systèmes fiscaux est un élément essentiel de notre intégration économique et de l'approfondissement du marché intérieur en Europe », a estimé Nicolas Sarkozy. La première étape de cette convergence devrait passer par un état des lieux des deux systèmes. La Cour des comptes s'en chargerait, côté français, un organisme équivalent s'y attelant outre-Rhin.

Le plan de rigueur allemand est soumis à des risques d'exécution

Le rapprochement franco-allemand en matière de fiscalité ressemble fort, côté français, à une volonté d'aligner le système fiscal sur le modèle allemand. Le poids des prélèvements obligatoires sur l'économie est globalement inférieur chez les deux plus proches partenaires de l'UE (42,8% du PIB en France et de 39,5% en Allemagne en 2008, selon les données énoncées par Nicolas Sarkozy ce mercredi), et leur répartition y est sensiblement différente (moins d'impôt direct, mais TVA plus forte

outre-Rhin)...

03 February 2010

A Comparison of Unemployment In the European Union and the United States

The EU has its Spain and Ireland. The United States has Michigan, Ohio, and Nevada.

23 February 2009

Europe to Push Broader Regulatory Agenda at G20

This is interesting because it tees up the European agenda ahead of the G20 meeting, and helps to highlight some points of contention between Europe and the Anglo-American financiers.

The IMF subject is a reflection of Europe's decentralized status. The ECB does not possess the broad powers of the Federal Reserve Bank, and there is a difference of opinion in Europe about its future role, and the centralization of power overall.

This is highly reminiscent of the US debate between the Federalists and the Jeffersonians.

MarketWatch

Europe supports broad financial regulation

By MarketWatch

12:42 p.m. EST Feb. 22, 2009

SAN FRANCISCO (MarketWatch) -- The European leaders of the Group of 20 called Sunday for more transparency and regulation of all financial markets, products and investors, including hedge funds, according to published reports.

Heads of state and finance ministers from France, Germany, Italy, the Netherlands, Spain, the United Kingdom, the Czech Republic and Luxembourg met in Berlin to come up with a European position ahead of the G20 summit in London scheduled for April 2...

Leaders also reportedly proposed increasing to $500 billion the International Monetary Fund's financial resources for crisis management, in light of problems recapitalizing banks in Central and Eastern Europe. The IMF now has $250 billion in resources and already used $50 billion.

The call for increased IMF funding follows remarks from French Finance Minister Christine Lagarde, who said Thursday that euro-zone countries should come to the aid of any troubled member-state and avoid IMF involvement, if a bailout becomes necessary....

Subscribe to:

Posts (Atom)